Risk and Reward in Investing

by Irish Life

Written by Irish Life staff

Guides • 27 March 2025 • 6 min read

You will learn:

The risks of investing your money.

The risks of NOT investing your money.

Finding the “right level” of risk for you.

The risks of investing: market downturns

The markets are a fickle beast, and no one can predict when the next swing will come – nor indeed which way that swing will go. Anyone who could accurately predict that would be unimaginably rich.

Market fluctuations happen in response to external factors from the economical to the geopolitical to the utterly unprecedented. A positive growth is known as a bull market, while a negative growth is called a bear market.

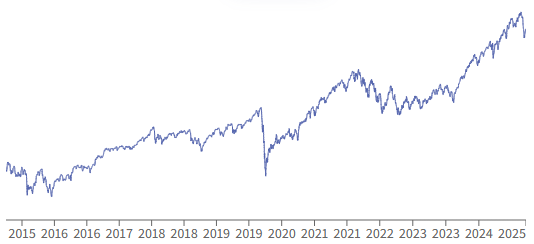

The graph below shows the performance of one of Irish Life’s Multi-Asset Portfolio (MAPs) funds over the past 10 years (late 2014 to early 2025).

MAPs 4 fund performance* from 2014 to 2025

Warning: Past performance is not a reliable guide to future performance.

You can see some significant dips, most notably in 2020 as the Covid-19 pandemic began in the west and in the wake of the political uncertainty following the Brexit vote and Donald Trump’s first election victory.

However, notice that outside of these large global events there are hundreds of smaller downturns across the period. While the graph is trending significantly upwards overall, an investor over a number of years in this fund would have experienced multiple weeks or months of losses on their way to returns.

Investment risk: unlucky timing

Timing the market is a fool’s errand – there’s an old saying that “time in the market beats timing the market.”

You can see for yourself in the MAPs graph above that someone who invested in January 2020 for the recommended minimum of five years would have seen a large return in spite of an initial significant drop.

Timing the market is impossible.

However, somebody who made a five-year investment in 2015 with a view to withdrawing returns in early 2020 would have nothing to show for it (and may have even lost money) by the time their five year plan ended.

Neither investor made a mistake with their five-year plan, but one of them was unlucky with timing.

Risks of investing: speculative investments

All investments carry risk, but some are far riskier than others.

As a general rule, making investments in something like a Multi-Asset Portfolio managed by a professional team is likely to be less risky than picking individual investments yourself.

Advantages of a managed Multi-Asset Portfolio include:

The investment is diversified, i.e. your money is invested in multiple assets (stocks, bonds, cash, property, alternatives) so that a downturn in one asset could be mitigated by upturns in others.

The fund is controlled by an investment manager who can adjust the investments based on market actions and predicted swings.

The volatility of any one company or government is less likely to severely impact your investment return.

The risk of not investing: inflation eats money!

We all know that investing carries risk. But have you considered that NOT investing could also be a risk?

One of the main advantages of investing over simply keeping the money in a relatively risk-free savings account (or even stashed under the bed!) is the potential for growth.

Sure, there is also the risk of losing money – but if you don’t invest, losing money isn’t just a risk: it’s virtually a guarantee.

Inflation is a fact of life. It’s a part of that old “supply and demand” concept that you don’t have to have an Economics degree to have heard of. Even though the recent cost of living crisis has given inflation a bad name, it’s actually the sign of a healthy economy when it’s steady and predictable.

However, that means that money will inevitably lose value.

Imagine you have €5,000 somewhere that won’t generate much of a return. It's either generating no interest, or significantly less interest than inflation.

An average inflation rate of 2.5% per year will see that €5,000 effectively worth just €3,882 in a decade.

Your €5,000 is of course still €5,000 – the money hasn’t vanished.

Inflation can wipe out savings.

But whereas you could buy €5,000 worth of goods and services with it 10 years ago, in this fictional future you can now only buy €3,882 worth of the same: the prices have gone up and your savings have stayed stagnant.

Had you invested that €5,000 and seen a modest 3.25% average annual return over that same decade, you’d have €5,344 instead. Despite inflation, you’d have more spending power than you started with.

Warning: These figures are estimates only. They are not a reliable guide to the future performance of your investment.

Opportunity cost: "investing is too complicated!"

One big reason that people in Ireland choose not to invest is the perception that investment is a complicated business. They’re much more comfortable just putting their money in a savings account, and so that’s what they do.

Too much information to absorb leads to low confidence, and unfortunately the world of finance and investments is often considered to be very complex.

Sure, what happens in the background of investment funds and financial markets can be very technical and intricate. But does that really matter?

You don’t need a doctorate in Economics to invest.

When you last bought a car, did you feel that you needed to understand compression ratios, injector pressures, torque, and ABS computer systems? Or did you just understand that some very expert people designed and built the engine in a way that makes the car work?

From your perspective, you just want to know the basics: what fuel does the car take? Is the brand reputable and reliable? Is there a good warranty?

There is no reason that choosing an investment should be any more difficult than choosing a car. You need to ask a few key questions and make one or two decisions, but after that it’s up to the experts.

Investing doesn't need to be complicated.

The relationship between risk and reward

As a very general rule, higher potential returns come with a higher risk of losses.

This is because risk and reward are two sides of the same coin, and that coin is named volatility. Volatility essentially refers to the size and frequency of the ups and downs an investment is likely to experience.

A stable, low-volatility investment is less likely to experience large downturns (but still could!) outside of those major global events that impact all markets. However, this investment is also far less likely to generate a significant return over time. Go too low-risk and your investment might not even beat inflation!

On the other hand, an investment with the potential for higher returns also comes with higher volatility. That means bigger swings and a bigger risk of ruin. Although a longer time in the market helps smooth out this volatility a little, it’s still a riskier investment than a lower-volatility choice - and any investment comes with the risk of losing money.

Your investment strategy and risk tolerance depends on you and your goals, and speaking to a financial advisor about investing will help you determine the investment volatility level you’re most comfortable with.

Warning: If you invest in this product you may lose some or all of the money you invest.

Warning: The value of your investment may go down as well as up.

Warning: These funds may be affected by changes in currency exchange rates.

- *Fund performance figures are before tax and after fund management charges on either our Signature 2 or Complete Solutions products. The Irish Property Fund is shown net of a 1% management charge.

- *Fund performance figures shown below are to a maximum of 10 years, to see fund performance since the fund launch date please see the fund’s factsheet. Fund factsheets provide general information and are a guide to the structure of a fund.

- *As funds are released in a number of series, fund charges and pricing may not match the series you're invested in. Login to your online account to see your fund information.

- *The fund management charges on other products may be different to those shown. For more information on fund charges please check your fund guide or product booklet.

What to read next

You may also like